So much for expensive homes, vehicles, and jewels. According to a recent survey conducted by Edward Jones and the nonprofit consumer education organization Life Happens, 81% of Americans consider their family to be their "most significant asset."

In addition, one-fourth of respondents in the adult national sample admitted that their biggest fear was burdening their loved ones with unforeseen financial obligations if they become incapacitated or pass away too soon. This raises the question :

Why don't more individuals purchase life insurance if we're so concerned about safeguarding what we value most?

Most experts will agree when you ask them that these plans can help give essential resources for anyone who has dependents to support. However, according to the most recent data, only 41% of American households have individual life insurance. According to Ken Cella, principal of the Client Strategies Group of the financial services company Edward Jones, "the majority of Americans have little to no safeguards for their financial aspirations." They may be aware of the importance of having emergency savings to handle unforeseen costs in the short term, but they lack protection against the financial consequences over the long run.

Even more frankly, Life Happens president Faisa Stafford states: "Emergency reserves aren't a long-term financial solution, especially if a family's main provider were to pass away." One or both of the following myths are to blame for a large portion of the discrepancy between what we'll refer to as "the need to protect" and the situation on the ground: * It's too expesive.

Think of this as the urban legend about alligators living in the sewers of New York City. In their 2017 Insurance Barometer Study, Life Happens and LIMRA, a global life insurance research and consulting group, asked participants to estimate the cost of a $250,000 term life policy for a healthy 30-year-old. According to NerdWallet, the median estimate was $500 per year, which is more than three times the actual annual amount of $160. However, suppose the prospective policyholder desired even greater protection for his dependents. A 20-year term policy with a million-dollar death benefit might be purchased by a healthy, non-smoking, 30-something male for $500, according to a recent calculation by Forbes magazine. Some folks spend more on caffe lattes than that each year. Nevertheless, costs can vary depending on your choice of term or permanent insurance, age, health, and the amount of coverage. The former, which is more economical, only lasts for a set period of time (often 20 years or less), but the later is perpetual (as long as you continue to pay the premiums). When deciding how much life insurance is right for you, there are a number of factors to take into account. Online tools like Edward Jones' free Life Insurance Needs calculator can help.

[PAKIBASA : Nandito po ang config. Hintayin lang po na matapos ang TIMER at pakipalo ang OPEN LINK BUTTON para lumabas ang link ng mga CONFIGS]

You have to wait 12 seconds

* The policy I have through work is good enough.

What if you're no longer working there?Group life insurance normally only offers benefits that are one or two times your yearly pay, and it is usually not transferrable. Growing families typically require more protection than that, according to Edward Jones financial adviser Scott Thoma, and they require insurance that is not dependent on employment status. Be aware that life insurance doesn't just give someone's life a dollar value. Which takes us to another another eye-opening result of the "Protect What Matters" poll conducted by Edward Jones and Life Happens. 23 percent of interviewees were unaware that it may even pay for a survivor's child's college bills.

Through Edward D. Jones & Co., L.P., as well as Edward Jones Insurance Agency of California, L.L.C., Edward Jones Insurance Agency of New Mexico, L.L.C., and Edward Jones Insurance Agency of Massachusetts, L.L.C., Edward Jones is a licensed insurance producer in all 50 states as well as Washington, D.C.

Although getting the right insurance may not be the most exciting aspect of owning a boat, it is important to use it wisely since it can help you avoid unnecessary costs, delays, and hassles in the event of an emergency. Boat owners should examine their existing plan, make sure they have the insurance that best suits their needs, and familiarize themselves with the fundamentals of the many forms of insurance coverage before a new boating season begins. This season, some important coverage regions to think about are as follows:

Salvage savvy

Nobody wants to lose a boat, but if it does, do not automatically believe that salvage is covered by your insurance. Some yacht insurers will deduct the cost of salvage from the boat's insured value, according to the Boat Owners Association of The United States (BoatUS). This implies that owners get less money for repairs or less money back if the yacht is a total loss. Therefore, look for a policy that includes salvage coverage that is distinct from and equal to the hull-value coverage.

Consequential concerns.

Boat insurance's problematic area is consequential damage. According to BoatUS data, roughly half of all sinkings take place when a tiny component below the waterline fails while the boat is docked, frequently as a consequence of wear and strain, corrosion, or poor maintenance. The failed part may not be covered by an insurance policy, but it must guarantee that it covers "consequential damage," such as significant repairs or the cost of the boat in the event of a total loss as a result of a failed part. Typically, catastrophic or entire losses are the only ones covered by this consequential damage coverage. For instance, it is common to pay for any immediate consequence damage brought on by any collision, stranding, demasting, fire, or explosion.

Rescue review.

Some boat insurance policies include on-water towing help; however, know which kind is best for your requirements. If you simply own one boat, find out from your insurance provider if it provides a towing service. Some businesses, like BoatUS, have their own fleet of towing vehicles. Important inquiries to make to your insurance provider:

Who is providing the towing service, if not their own fleet ?

Is there 24-hour service?

Will you have to pay out of pocket and seek reimbursement

For more tips and information to optimize your boat insurance, visit BoatUS.com/insurance for quotes or contact marine insurance specialists at 800-283-2883.

It is "a game-changer," and with good reason. Today, major medical insurance, Medicare, workers' compensation, and even certain Medicaid programs commonly cover the costs of chiropractic care for tens of millions of Americans.

According to studies, chiropractic care can cut expenses each episode of care by as much as 40%. And given that musculoskeletal diseases cost more than $700 billion to treat in just 2011, savings of this magnitude and chiropractic care's better reported patient satisfaction should be commended.

Feel free to bring your insurance card with you when you visit your chiropractor.

Every year, almost 30 million Americans seek chiropractic care, but it seems that not all of them are aware that most major medical insurance companies, Medicare, workers' compensation, and even some Medicaid plans typically pay these visits. The Patient Protection and Affordable Care Act's anti-discrimination provisions and the government's general acceptance of chiropractic care at all levels, including military bases and Veterans Administration facilities, both contributed to the expanded accessibility.

Increasing awareness, according to experts, might shift the game.

Think about this According to the most recent data available, musculoskeletal illnesses accounted for one of the most expensive healthcare expenses in 2011 with more than $796 billion spent on their treatment. In the meantime, multiple studies have demonstrated that the "chiropractic-first" strategy that many specialists promote—avoiding traditional spine surgery and potentially addictive drugs—is friendlier to both wallets and patients.

Chiropractic care has been shown to result in better clinical outcomes and overall higher patient satisfaction, according to Sherry McAllister, DC, executive vice president of the nonprofit Foundation for Chiropractic Progress. "Chiropractic care is documented to reduce costs per episode of care by up to 40%," she adds.

Chiropractic doctors, who must complete seven years of college, use a hands-on method to treat neuro-musculoskeletal disorders such back, neck, and joint discomfort.

Doctors of chiropractic are primary care providers for spine health and wellbeing who are committed to providing Americans with conservative care as an alternative to the misuse, abuse, and dependence on opioids that results from prescription medication usage. Visit F4CP.com to learn more.

Insurance is a means of protection from financial loss. It is a method of risk management that is primarily employed to protect against the risk of a potential loss.

An organization that offers insurance is referred to as an underwriter, insurer, insurance business, or insurance carrier. An insured or a policyholder is a person or thing that purchases insurance. In exchange for the insurer's pledge to pay the insured in the case of a covered loss, the insured agrees to assume a guaranteed and known, relatively small loss in the form of payment to the insurer. The loss could be financial or not, but it must be measurable in terms of money. It typically involves something in which the insured has an insurable interest, which can be proven by ownership, possession, or a previous connection.

A contract known as an insurance policy is given to the insured outlining the terms and circumstances of the insurer's obligation to pay the insured. The premium is the sum of money the insurer charges the policyholder in exchange for the protection outlined in the insurance policy. The insured makes a claim to the insurer for processing by a claims adjuster if they sustain a loss that may be covered by the insurance policy. A deductible is an obligatory upfront cost imposed by an insurance policy prior to the insurer paying a claim (or if required by a health insurance policy, a copayment). By obtaining reinsurance, which involves another insurance company agreeing to assume part of the risks, the insurer can reduce its own risk, especially if the primary insurer determines that the risk is too great for it to bear.

Insurance companies may sell any combination of insurance types, but are often classified into three groups:

Companies that sell products like life insurance, annuities, and pensions that are related to asset management enterprises are called life insurance companies.

firms that sell property/casualty insurance or non-life insurance.

Health insurance providers that sporadically offer life insurance or employee perks

General insurance companies can be further divided into these sub categories.

Standard lines

Excess lines

Life and non-life insurers are typically subject to various regulatory frameworks, as well as different tax and accounting regulations. The fundamental distinction between the two types of businesses is due to the very long-term nature of the life, annuity, and pension business; insurance for life or a pension can cover risks over many decades. Non-life insurance coverage, in contrast, typically covers a shorter time frame, such as one year.

Mutual versus proprietary

Insurance providers are typically categorized as mutual or proprietary businesses. While stockholders (who may or may not own policies) own proprietary insurance firms, policyholders own mutual insurance businesses.

In several nations, including the United States, demutualization of mutual insurers to create stock corporations and the creation of a hybrid known as a mutual holding company became widespread in the late 20th century. Not all states, meanwhile, allow joint holding companies.

Reinsurance companies

Reinsurance firms are insurance firms that offer policies to other insurance firms so that they can lower their risks and guard against significant losses. A small number of very big corporations with enormous reserves control the majority of the reinsurance market. A direct writer of insurance risks might also be a reinsurer.

Captive insurance companies

Limited-purpose insurance firms with the specific goal of financing risks arising from their parent organization or groups are known as captive insurance companies. This term can occasionally be expanded to encompass some of the hazards associated with the clients of the parent company. It is, in essence, a form of internal self-insurance. A "mutual" captive insures the collective risks of members of an industry; a "association" captive self-insures the individual risks of the members of a professional, commercial, or industrial association; or a "pure" entity, which is a wholly owned subsidiary of the self-insured parent firm. Because of the cost reductions they contribute to, the simplicity of insurance risk management, and the flexibility for cash flow they produce, captives bring commercial, economic, and tax advantages to their sponsors. Additionally, they might offer affordable coverage for risks that are neither available nor offered in the conventional insurance market.

Property damage, public and product liability, professional indemnity, employee benefits, employers' liability, automobile and medical aid charges are just a few of the risks that a captive can underwrite for their parents. The use of reinsurance may help to reduce the captive's exposure to such risks.

The role of captives in their parent's risk financing and management strategy is becoming more and more crucial. When considered in light of the following context, this is clear:

Heavy and increasing premium costs in almost every line of coverage

Difficulties in insuring certain types of fortuitous risk

Differential coverage standards in various parts of the world

Rating structures which reflect market trends rather than individual loss experience

Insufficient credit for deductibles or loss control efforts

Other forms

Reciprocals, in which policyholders reciprocate by sharing risks, and Lloyd's organizations are two additional configurations for an insurance firm.

Admitted versus non-admitted

Insurance companies in the United States that have been accepted or granted a license by the state licensing body are known as acknowledged insurance companies. They market accepted insurance as their product. When admitted firms are unable or unwilling to fill a need for insurance, non-admitted companies are permitted to provide insurance under particular circumstances despite not having received state licensing agency approval.

Insurance consultants

There are organizations referred to as "insurance consultants." These businesses receive a charge from the customer to research various insurance policies from different firms, much like a mortgage broker. An "insurance broker" works with numerous insurance firms to get the best insurance policy, much like an insurance consultant. However, with insurance brokers, the payment is typically made through a commission from the chosen insurer rather than by the client.

[PAKIBASA : Nandito po ang config. Hintayin lang po na matapos ang TIMER at pakipalo ang OPEN LINK BUTTON para lumabas ang link ng mga CONFIGS]

Hintayin matapos ang timer, kapag may

pop-up ads ay i-back lang. Pasensya agad, need yan para manatiling buhay ang website at patuloy makapag update ng config.

You have to wait 12 seconds

Insurance transactions do not transfer any risks to insurance consultants or brokers because neither are insurance firms. Firms known as third party administrators provide insurance companies with underwriting and occasionally claims management services. These businesses frequently possess specialized knowledge that insurance firms do not.

Financial stability and rating

When purchasing an insurance contract, the strength and stability of the insurance provider should be taken into serious consideration. A current insurance premium provides protection against losses that could occur many years in the future. The insurance company's viability is crucial because of this. Several insurance businesses have gone bankrupt in recent years, leaving their consumers without coverage (or coverage only from a government-backed insurance pool or other arrangement with less attractive payouts for losses). Information is provided and the financial viability of insurance businesses is rated by a number of independent rating agencies.

Several organizations, including A. M. Best, rate insurance companies. The company's financial strength, which gauges its capacity to settle claims, is factored into the ratings. Bonds, notes, and securitization products, among other financial instruments issued by the insurance firm, are also rated.

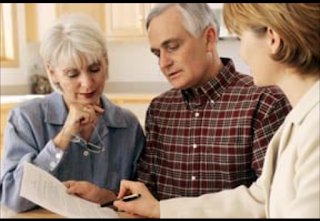

Complete Value Of Life Insurance And Working With A Financial Professional

Planning for retirement has not been easy over the past few years. Saving and investing for a secure financial future have become more difficult than ever because of market instability, declining real estate values, and for others, job loss or stagnant earnings. A financial expert can help in this situation.

A financial expert can assist you in making financial decisions that will protect the things that are important to you, such as your family, your business, or your way of living. But how can you identify a financial expert who is a suitable fit for you?

1. Start by considering his or her philosophy and approach to retirement planning. In today’s tenuous financial environment, a professional who believes permanent life insurance plays a critical role in a financial plan should be a strong consideration. Permanent life insurance provides a guaranteed safety net, should the unthinkable happen. A death benefit can give you peace of mind that your family or business is properly protected. Plus, the cash accumulation potential of permanent life insurance can be used to launch a second career, pay for a grandchild’s education or supplement retirement revenue streams. Permanent life insurance also allows other elements of a financial plan, such as annuities, investments or disability insurance, to do their job.

2. Make sure the financial professional has the proper education and training. Here are the top credentials to look for:

Chartered Life Underwriter (CLU) — an insurance designation often held by those who specialize in life insurance and estate planning and given by The American College, a nonprofit dedicated to educating individuals in financial services.

Certified Financial Planner (CFP) — a designation given and governed by the Certified Finacial Planner Board of Standards.

Chartered Financial Consultant (ChFC) — a designation on par with the CFP, also given by The American College.

3. Make certain you have a good comfort level with the financial professional, and how they communicate with clients. You can do this by scheduling an in-person meeting, preferably at their office, to ask the following questions:

What is your approach to retirement planning?

How often will I have the opportunity to meet in person to make sure my plan can adjust as my life evolves?

What is the average length of your relationships with clients?

Will you offer options and help me compare risks, costs and benefits?

How will you communicate with me about my finances?

All guarantees are based on the claims paying ability of the issuer. Accessing cash-values may result in surrender fees and charges, may require additional premium payments to maintain coverage and will reduce the death benefit and policy values. Any examples are hypothetical, intended for illustrative purposes only, and highlight a single possible outcome. Individual results will vary.

To learn more about working with a financial professional to take full advantage of the complete value of life insurance, visit www.PennMutual.com.

[PAKIBASA : Nandito po ang config. Hintayin lang po na matapos ang TIMER at pakipalo ang OPEN LINK BUTTON para lumabas ang link ng mga CONFIGS]

Hintayin matapos ang timer, kapag may

pop-up ads ay i-back lang. Pasensya agad, need yan para manatiling buhay ang website at patuloy makapag update ng config.

You have to wait 12 seconds

Life Insurance: Possibilities In A New And Complex World

Only 44% of American families had individual life insurance in 2016, and 30% of those homes had no coverage at all, according to a recent research by the Life Insurance and Market Research Association.

These figures come at a time when it has never been more sensible to use life insurance for both its protection advantage and as a tool to accumulate wealth. Home ownership, defined benefit plans, 401(k) matches, and social security were once pillars of financial security but are now in jeopardy. These conditions make it difficult to use many of yesterday's financial solutions to support a college degree, start a new business, or deal with an unanticipated health issue.

Regularly evaluated and updated permanent life insurance policies safeguard more than just financial assets. It provides stability and enables you to benefit from a wide range of life's opportunities.

Here are some typical myths you should be aware of if you're thinking about purchasing life insurance or raising the amount of coverage you currently have:

Life insurance only provides a death payout. Permanent life insurance enables cash value accumulation in addition to a death payout. You and your family or small business can utilize this money to pay for a variety of living expenditures.

The best course of action is to purchase term insurance with a minimal death benefit and invest the remaining funds in other ventures. Death protection is crucial, but permanent life insurance provides both that protection and cash-building potential, fitting your needs as they change over the course of your lifetime.

Only if you have children does life insurance become important. Aside from safeguarding children, life insurance can meet a variety of needs. For example, you may use the cash value of a permanent policy to support a charitable cause you care about or expand your business.

Life insurance is a recurring expense. A permanent life insurance premium payment is an investment in your future. As a permanent policy builds up monetary worth over time that may be accessed whenever and however is necessary, it functions similarly to paying yourself.

Please visit www.pennmutual.com for more details about all of the life's potentials that life insurance may satisfy.

When you're young, you frequently disregard perfectly good advice that is given to you on a range of subjects. Consider buying a permanent life insurance policy early in your working life, while you're young and healthy, is one piece of advise that shouldn't be disregarded.

Too many American youth only contemplate the death benefit of life insurance, ignoring its other benefits and full worth. Although it accumulates cash value that policyholders can use to pay for college, put a down payment on a house, or use as a significant source of income for any other purpose throughout their lifetime, permanent life insurance offers vital death benefit protection.

The advantages of buying a permanent life insurance policy at age 25 versus age 40 are startlingly different.

By investing a little over $180 a month in a Flexible Choice Whole Life insurance policy, a 25-year-old female will have more than $29,000 in guaranteed cash value by the time she turns 40. By the time she turns 65, the guaranteed cash value will have increased to $120,600 and will have a guaranteed death benefit of $300,000.

This female would have had just over $53,000 in guaranteed cash value at age 65 and a death benefit of $161,000 if she had waited until age 40 to start making the same monthly payment into a Flexible Choice Whole Life policy. (Nearly half of the amount she could have purchased if she had waited until she was 25.)

A financial expert will create a plan specifically for you based on your financial objectives and show you how permanent life insurance works with a good financial strategy.

1. Reducing the death benefit and policy values by accessing cash values may result in surrender fees and charges, additional premium payments to keep coverage in place, and other costs.

2. Assumptions: female, age 25, preferred non-smoker, monthly premium of $183, death benefit of $300,000.

3. Hypotheses: 40-year-old female, non-smoker, preferred, monthly premium of $183, death benefit of $161,503. only considers a slight decrease in health rating. A further change in health would result in a higher premium or make coverage unavailable.

Visit www.Pennmutual.com to find out more about the advantages of beginning a financial plan that includes permanent life insurance and the actual rewards of doing so.

Minimize Retirement Risk With Permanent Life Insurance

Many Americans worry about their retirement due to ongoing economic uncertainties. Workers may be troubled by the potential of a retirement where the notion of not having enough money may not be hyperbole rather than daydreaming about their senior years. Consumers want to reduce risk and take charge. A financial advisor will customize a strategy to match each person's unique financial objectives, but every diversified retirement strategy should include permanent life insurance because it can provide security and growth for individuals who still have a number of working years ahead of them. Permanent life insurance offers both the possibility of accumulating cash values, which can be a significant source of retirement income, and death protection. Cash from a permanent insurance policy may be used for any purpose as its value increases over time tax deferred. In addition to supplementing other income sources like Social Security, 401k savings, or pensions for those who are fortunate enough to have them, this type of life insurance offers consumers a certain amount of flexibility that empowers them to make decisions and better manage their financial lives. The "gap years" that occur between retirement and the age at which Medicare and Social Security benefits start may also be covered in part by the income stream from a perpetual life insurance policy.

The majority of retirees will want the assistance of a financial expert to decide how best to allocate their resources during the transition period and during retirement. Consumers should be aware, though, that a permanent insurance coverage can mean the difference between retiring when you want to rather than when Social Security and qualifying plan dividends begin. A retiree may also be able to put off the start of receiving Social Security benefits, which would eventually result in bigger monthly payments over time.

A perpetual insurance policy may help cover unanticipated or planned expenses such as healthcare costs, the cost of a grandchild's college education, or the start-up of a family business in addition to aiding in bridging the gap years. No matter how permanent insurance is ultimately used, if a policy is properly constructed, it can offer a death benefit that is both income tax and estate tax free. Retirement income can then be spent with the assurance that a legacy will be left to one's children or a preferred charity.

To learn more about how to leave a legacy and strengthen your retirement plan with permanent life insurance, please visit www.pennmutual.com.

Savvy Financial Planning Sooner Means More Money Later

Whether you are new to the workforce or a seasoned pro, retirement planning is the secret to long-term wealth, and it is never too early or too late to make a plan to live your best life in later years. With the unique challenges and unpredictability caused by the coronavirus pandemic, many people were forced to neglect or ignore their savings and financial planning. That’s certainly understandable. But as the economy improves, new workers and those approaching retirement can take advantage of smart ways to plan and save in a way that they may not have been able to a year ago. The following tips from CFP Board, a nonprofit organization dedicated to benefitting the public by supporting professional standards in personal financial planning, may give you some ideas on how best to plan for your retirement:

Go high-tech, with caution. "Keeping track of your personal finances is time-consuming and not what you want to do in your retirement years," says CFP Board Ambassador Bill Schretter, CFP®.

"I recommend all my clients automate as much of the saving and reporting functions as possible. However, I do not recommend that you use free service apps," he emphasizes.Why? Many free service apps will use your information to try to sell you financial and non-financial products that you don’t need and could siphon away from your retirement savings."I recommend that you purchase your own program or use programs that your advisor or bank provide to help you keep your finances organized," says Schretter. "Let an app automate regular tasks, but leave the most important financial advice and management to qualified human beings," he adds.A CERTIFIED FINANCIAL PLANNER™ professional can provide guidance as you consider these points in retirement planning, whatever your current work status or age:

Review your goals. Does your retirement wish list include a cruise to Alaska, an African safari, or your own house on a secluded lake in the woods? Do you want to open a small business, or help out your children and grandchildren with education costs? Consider potential expenses now to plan savvy withdrawals later.Watch for tax traps. "If your withdrawal plan puts you into a higher tax bracket, you might want to lower the amount you plan to pull out," says CFP Board Ambassador J.J. Burns, CFP®.

Also, diversify with a range of accounts that are taxed differently for more flexibility. If you don’t have a Roth IRA or 401k, it is never too early or too late to start one, and a certified financial planner can give advice on moving some retirement savings into one of these accounts to maximize future income. Visit LetsMakeAPlan.org for more advice and tips to make the most of your income in retirement.